[ad_1]

After 13 years with negative real returns on savings on average, it’s time to demand that the Fed tackle its impact on savers.

Through Alex J. Pollock, principal investigator at the Mises Institute.

With inflation exceeding 6% and interest rates on savings close to zero, the Federal Reserve is offering a negative 6 percent real (inflation-adjusted) return on trillions of dollars in savings. It is indeed a question of expropriating the pips of American savers at a rate of 6% per year.

However, this is not just a problem in 2021, but a persistent and long-standing monetary policy problem. The Fed has been delivering negative real returns on savings for more than a decade. He should discuss with the legislator what he thinks of this result and its impact on savers.

The effects of central bank monetary actions pervade society and transfer wealth between various groups of people – political action. Monetary policies can cause consumer price inflations, as they are now, and asset price inflations, like the ones we have for stocks, bonds, houses, and cryptocurrencies. They can feed bubbles, which turn into busts. They can, through negative real returns, push savers into stocks, junk bonds, houses, and cryptocurrencies, temporarily inflating prices further while increasing risk significantly. They can withdraw money from conservative savers to subsidize leveraged speculators, thus encouraging speculation. They can transfer the wealth of the people to the government through the inflation tax. They can punish savings, prudence and autonomy.

Savings are essential for long-term economic progress as well as personal and family financial well-being and responsibility. However, the policies of the Federal Reserve, and those of the government in general, have subsidized and accentuated the expansion of debt, and unfortunately seem to have forgotten about savings. The original theorists of the savings and credit movement, to their credit, were clear that “savings” were required first to make “loans” possible. Our current unbalanced policy could be described, instead of “savings and loansâ€, as “loans and loansâ€.

In the immediate term, Congress should require the Federal Reserve to provide a formal analysis of the impact on savers as part of its Humphrey-Hawkins reports on monetary policy and targets. This saver impact analysis must quantify, discuss and project for the future the effects of the Fed’s policies on savings and savers, so that these effects can be explicitly and equitably taken into account along with the other relevant factors. .

The critical questions are: What impact does the Fed’s monetary policy have on savers? Who is affected? How will the Fed’s monetary policy plans affect savings and savers going forward?

Year-over-year consumer price inflation in October 2021 stands, as we painfully know, at 6.2%. For the ten months of 2021 since the start of the year, the pace is even worse than that – an annualized inflation rate of 7.5%.

Faced with this inflation, what are the returns of savers of all kinds, but in particular retirees and savers of modest means, who reap on their savings? Basically nothing.

According to the Federal Deposit Insurance Corporation’s National Interest Rate Report of October 18, 2021, the national average interest rate on savings accounts was 0.06%. On money market deposit accounts it was 0.08%; on three-month certificates of deposit, 0.06%; on six-month CDs, 0.09%; on six-month Treasury bills, 0.05%; and if you’ve committed your money over five years, a majestic 0.27 percent CD rate.

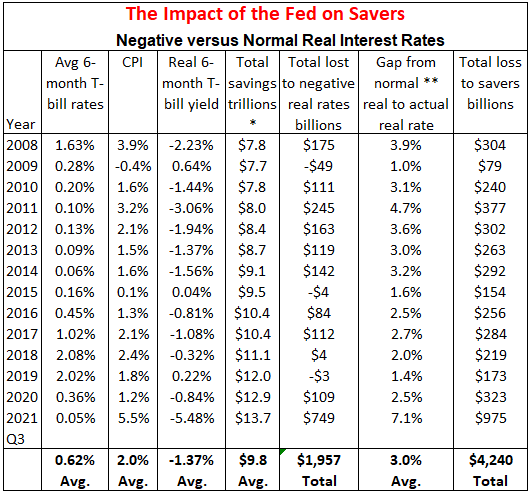

I estimate, as the table below shows, that monetary policy since 2008 has cost US savers about $ 4 trillion.

The table assumes that savers can invest in six-month Treasury bills and then subtract the corresponding inflation rate from their average interest rate, giving savers the real interest rate. It is on average quite negative for these years. I calculate the amount of savings effectively expropriated by negative real rates. Next, I compare the real real interest rates to an estimate of the normal real interest rate for each year, based on the fifty-year average of the real rates from 1958 to 2007. This gives us the spread that the Federal Reserve has created between real real rates in the years since 2008 and what would have been historically normal rates. This gap is multiplied by household savings, which arithmetically shows us the total gap in dollars.

* Total household savings are made up of term and savings deposits, units of money market UCITS and treasury bills

** Normal real rate is the average of 6-month Treasury bill yields less CPI inflation, 1958-2007, = 1.66%

Sources: Federal Reserve Statistical Release, United States Financial Accounts – Z.1, United States Bureau of Labor Statistics, Consumer Price Index for All Urban Consumers: All articles in city average US and Federal Reserve System Board of Governors (United States), secondary market rate on 6-month Treasury bills

To repeat the answer: a $ 4 trillion blow to savers.

The Federal Reserve, through regular saver impact analysis, is expected to have in-depth discussions with Congress on how its monetary policy affects savings, what are the resulting real returns for savers , who are the resulting winners and losers, what are the alternatives and how his plans will impact savers in the future.

After thirteen years with negative real returns on average for conservative savings, it’s time to demand that the Federal Reserve tackle its impact on savers. By Alex J. Pollock, Senior Fellow at the Mises Institute.

Do you like reading WOLF STREET and want to support it? Use ad blockers – I totally understand why – but you want to support the site? You can donate. I really appreciate it. Click on the beer and iced tea mug to find out how:

Would you like to be notified by email when WOLF STREET publishes a new article? Register here.

![]()

Classic Metal Roofing Systems, our sponsor, manufactures beautiful metal shingles:

- A variety of resin-based finishes

- Deep grooves for a premium natural look

- Maintenance free – won’t rust, crack or rot

- Resists scratches and smudges

To reach the Classic metal roof people, Click here or dial 1-800-543-8938

[ad_2]